Are we responsible consumers?

Yes, I’m talking about you and me. How are we doing, collectively, at managing our income and spending?

The question came to mind when the New York Federal Reserve Bank released the most recent figures on consumer debt earlier this month. If you look at the gross numbers, our debt is scary, some $18.20 trillion at the end of March. That’s up a whopping $4 trillion since the end of 2019, just before the pandemic started.

Collectively, we’ve increased our mortgage debt. We borrowed more against our home equity credit lines.

But we reduced our credit card debt. And believe it or not, we decreased our automobile debt.

The Prudence Test

The test of prudence, however, isn’t how many trillions we owe.

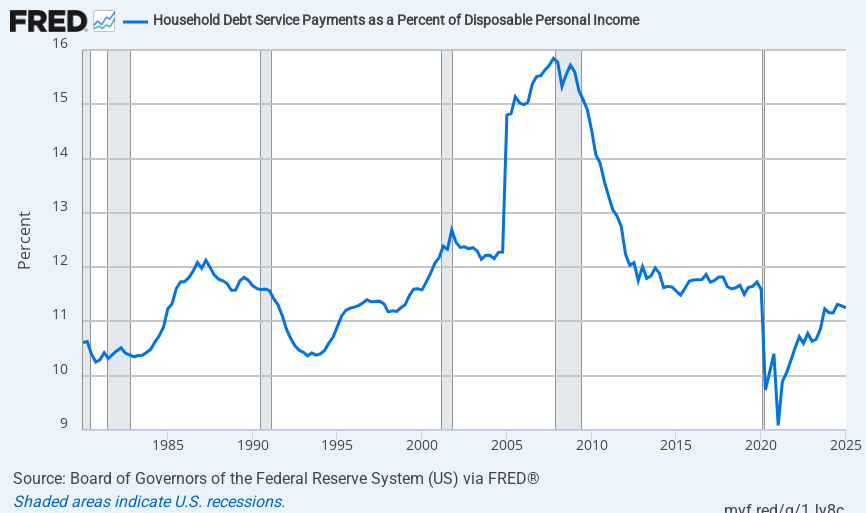

It’s how much of our income goes to making payments on our debts. If it’s a crushing burden, we’re in trouble. If it’s easily handled, we’re fine.

That’s where FRED, the huge graphical database maintained by the Federal Reserve Bank of St. Louis, comes in handy. Its quarterly updated chart shows household debt service payments as a percent of disposable personal income ended 2024 at only 11.28 percent of disposable personal income – our income after taxes and other required payments.

This is down slightly from 11.72 percent at the end of 2019. It’s down massively from the 15.85 percent recorded at the end of 2007, the peak of the housing bubble.

The last time our debt service was at this level was the end of 1998.

This doesn’t mean we’re all prudent borrowers.

There are people out there with huge student loans, multiple auto loans and impressive mortgage payments. Just as you can drown in a Texas creek with an average depth of a few inches if you step in a rare deep spot, some households will always be pushing the limits for debt.

But we shouldn’t forget about all the households with little or no mortgage debt – about 40 percent. And no credit card debt – about 52 percent. While some households need credit cards to pay regular bills, a larger group uses credit cards for transactions and pays everything off monthly.

Us vs. Congress

Now let’s check how our elected friends and helpers are doing in Washington. According to a regular report by the Peter G. Peterson Foundation, federal interest payments will be 18.4 percent of federal revenues by the end of 2025. They will reach 22.2 percent by 2035.

Another Peterson Foundation paper examines how four major institutions score the “One Big Beautiful Bill Act” — President Trump’s tax bill. All four concluded it would increase federal debt to over $50 trillion within 10 years. This will further increase interest expenses as a percent of federal revenues.

Growth Isn’t “The Cure”

Treasury Secretary Scott Bessent has said that we’ll grow our way out of the current deficit. Everything will be hunky dory. Growth cures all.

That, strangely, is exactly what then Congressman, now Senator, Edward Markey (D., MA) told economist Laurence J. Kotlikoff in 1999 when the two found themselves sitting next to each other on a flight to Washington DC.

“You ivory tower guys worry too much,” Markey told Kotlikoff.

“The economy is growing like crazy. Technological progress has never been this rapid. Do you have any idea what’s going on in high tech? We’re going to outgrow these financial problems. It’s time to get real.”

But it didn’t turn out that way, did it?

You may recall, even if the 535 who purport to represent us don’t.

A few years later the entire dot.com boom was a bust. Billions in investment went down the tubes. The expected huge growth never appeared.

The reality here is that we American consumers – Citizens! — are more financially responsible than the people we elect, regardless of party.

Spending gives them power. Always has, always will. And they will borrow whatever they need to keep that power.

We need to learn that lesson.

Will the Responsible Party please stand up?

Related columns:

Scott Burns, “The Supreme Grand Poohbah Saves Social Security,” 5/4/2025: https://scottburns.com/the-supreme-grand-poohbah-saves-social-security/

Scott Burns, “Taxes and the Consumer Price Index,” 1/26/1997: https://scottburns.com/taxes-and-the-consumer-price-index-2/

Sources and References:

FRED: “Household Debt Service Payments as a Percent of Disposable Personal Income,” https://fred.stlouisfed.org/series/TDSP

Fidelity.Com: “What is disposable income?”: https://www.fidelity.com/learning-center/smart-money/disposable-income

Consumer debt figures: New York Federal Reserve, Quarterly Report on Household Debt and Credit, Q1, 2025: https://www.newyorkfed.org/medialibrary/interactives/householdcredit/data/pdf/HHDC_2025Q1

Axios.com: “A record share of U.S. homes are mortgage-free,” 12/12/2013: https://www.axios.com/2023/12/12/mortgage-free-homes

Bankingexchange.com: “48% of Credit Cardholders Carry Debt from Month to Month,” 1/13/2025: https://www.bankingexchange.com/news-feed/item/10203-48-of-credit-cardholders-carry-debt-from-month-to-month

Federal debt figures: The Peter G. Peterson Foundation, “The Scorekeepers Agree: Budget Bill will Increase U.S. Debt by Trillions,” 6/6/2025: https://www.pgpf.org/article/the-scorekeepers-agree-budget-bill-will-increase-u-s-debt-by-trillions/

Federal debt figures: The Peter G. Peterson Foundation, “Interest Costs on the National Debt,” https://www.pgpf.org/programs-and-projects/fiscal-policy/monthly-interest-tracker-national-debt/

Consumer Price Index: Bureau of Labor Statistics, May CPI, released 6/11: https://www.bls.gov/news.release/pdf/cpi.pdf

Laurence J. Kotlikoff, “Fiscal Child Abuse,” 5/27/2025: https://larrykotlikoff.substack.com/p/fiscal-child-abuse

Tax Foundation, “Did 1997 Capital Gains Tax Exclusion for Housing Contribute to Economic Crisis?,” 9/25/2008: https://taxfoundation.org/blog/did-1997-capital-gains-tax-exclusion-housing-contribute-economic-crisis/

This information is distributed for education purposes, and it is not to be construed as an offer, solicitation, recommendation, or endorsement of any particular security, product, or service.

Photo by adrian vieriu: https://www.pexels.com/photo/a-close-up-shot-of-dollar-bills-11624965/

(c) Scott Burns, 2025

4 thoughts on “Are We Responsible Consumers?”

Comments are closed.

Yesterday the U.S. Senate used an accounting budget lie to pass its version of Trump’s “One Big Beautiful Bill Act.” If the U.S. House passes its version of the bill, how long will it take global bond traders to begin reacting? What actions, if any, should a middle-class, Couch Potato investor take?

The bond market is already uneasy, so it’s not a matter of when but how much more reaction are we likely to see. Since the tariff issue is likely to reduce the need for other nations to hold Treasuries as well as their trust in them, every negative (such as rising energy prices, further decline in consumer confidence vis-a-vis inflation, job security, etc. is likely to be amplified.

What to do is another matter. The prudent thing is to shift to shorter average maturity on the fixed income side of the Couch Potato portfolio. Another action, which requires more work right now but very little afterwards, is to create a ladder of Treasury Inflation Protected Securities that will cover needed distributions over the next 5+ years. This can easily be done using an iShares ETF series. You can learn about them here:

https://www.blackrock.com/us/financial-professionals/investments/products/ibonds?cid=ppc:uswa_us:uswa_us_nb_ibonds_product_phrase_fa:google:nonbrand_prod:fa&gclsrc=aw.ds&gad_source=1&gad_campaignid=22433562475&gbraid=0AAAAADrFitPS0wzAPB4AOk2kt1YkGDMwL&gclid=CjwKCAjwsZPDBhBWEiwADuO6y38JSEKmMd0g6yXhYnj-4s-u6zAdR_DZStMR2jwzNAEegVy_l7f3xRoCFnoQAvD_BwE

Thanks, Scott. Your clear response is very much appreciated.

It is hard to accept that Consumers are more Responsible than our Elected Official. Thanks for pointing this out. I vote for less spending and more taxes to at least balance the budget. I only think of Growth as a bonus to cure our defecit.