They say context is everything.

Bear that in mind as we consider how the financing of Social Security, once considered a huge problem, has become, well, kind of a small thing. Relatively.

Yes, I know this is hard to believe. But be patient. I’ll explain. It makes sense in a dark, terrible way.

I’ve reported for years about the projections for the exhaustion of the Social Security trust fund. After the 1984 reforms, which were supposed to solve the problem, the event was predicted for late in this century. But it has been edging closer year by year. In the 2025 trustees report, it was projected for 2033.

Just seven years from now.

At that time, the report said the“continuing program income will be sufficient to pay 77 percent of total scheduled benefit.” That, you should know, was the “intermediate” projection. Another says it will take longer. Still another says it will be as early as 2031.

Just five years from now.

Unless you’re in the “My retirement will be fine as long as I die by Friday” crew, that’s rather close at hand.

The Optimism of the Actuaries

You should also know that the trustees and their actuaries are surprisingly optimistic. No one knows how that happened. It’s not what actuaries are about.

I’m serious. Skeptics should check with Andrew Biggs. He’s a senior fellow at the American Enterprise Institute. He likes poking holes in sacred cows. In a recent Substack piece, Biggs noted that the trustees were magically assuming a fertility rate of 1.9 children per woman going forward, while the most recent actual rate is 1.6.

When considering the future of humanity, that’s a big difference.

Other institutions are projecting, at best, a continuation of 1.6. Personally, I’ve always felt that humans were fortunate that conceiving children was so much easier than sustaining adult relationships. Were conception more difficult, our species would have disappeared long ago. Today, entire nations seem to have lost the knack for conceiving.

(You can read Biggs post here: https://substack.com/home/post/p-194091246 )

Following the Money

But let’s get back to the money and the coming shortchanging of retirement.

While most of the regular press takes the information releases from Social Security seriously by repeating the warnings about how the Social Security trust fund will be depleted by 2033 or 2031, the reality is that our surplus contributions were deposited to the U.S. Treasury in exchange for IOUs. The Treasury then dutifully distributed the actual cash to be spent by our friends in Congress. The trustees also dutifully accrued interest on the IOUs in the hallowed trust fund.

But if you examine the finances of Social Security without counting interest payments, what you learn is that the cash expenses of the program have exceeded the cash revenue of the program (including taxation of benefits) since 2010.

Since then, the excess expense has grown year after year. One clue is the rapidly shrinking size of the Social Security trust fund.

Congress Shrinks the Social Security Problem By Making a Much Bigger Problem

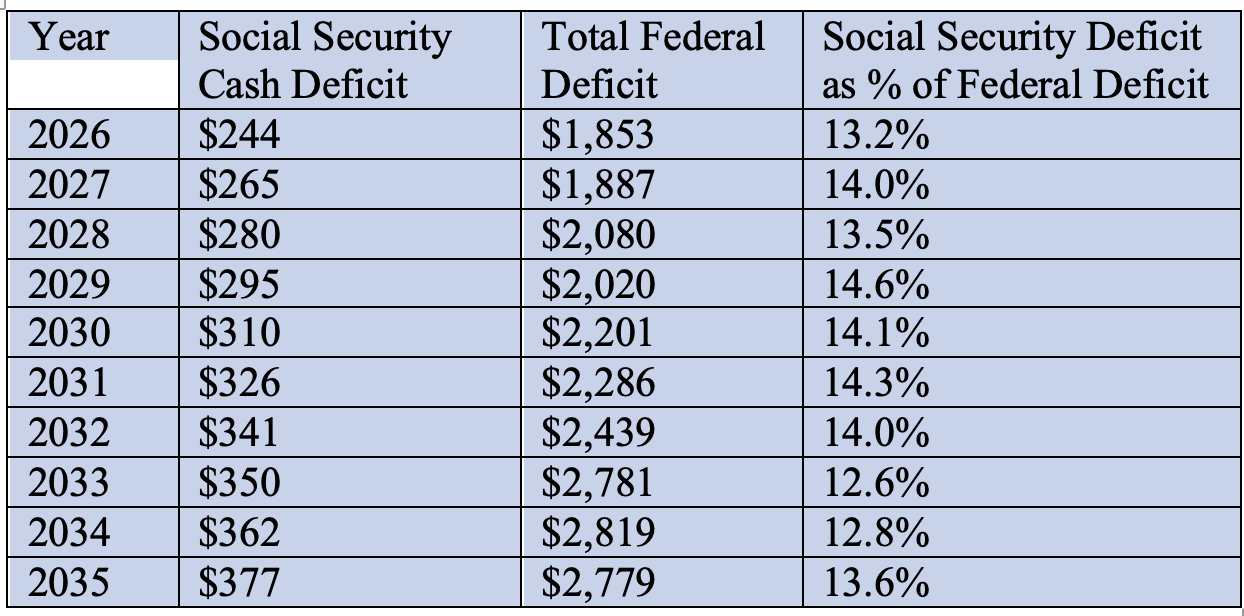

Fortunately, we can get to the Truly Big Picture with a very direct exercise. To do it, we’ll need to compare the figures in two reports.

—The first will be the cash deficit projected by the Social Security Trustees over the next 10 years.

—The second will be the total federal deficit projected by the Congressional Budget Office over the same period. This figure includes the Social Security deficit.

Once a terrifying number, worth exhortations from Republicans who talked in serious tones about “fiscal discipline” and “responsible spending,” the cash shortfalls of Social Security are now minor when compared to the total annual federal deficit.

According to the February report on “The Budget and Economic Outlook: 2026 to 2036” published in February, the total federal deficit for 2026 will be $1,853 billion. It is expected to rise to a whopping $2,779 billion by 2035.

Making a Big Deficit Seem Small

Sources: https://www.ssa.gov/oact/TR/2025/VI_A_cyoper_hist.html#282924 , https://www.cbo.gov/publication/62105#_idTextAnchor005

At one time, a cash shortfall of $244 to $377 billion would have been impressive. Today it is more than a footnote. It’s also more than governmental rounding error. But it has become a complete sideshow to the big deal, the gigantic federal deficit.

Actually, It’s Already Worse Than That

Still worse, these figures are already wrong. Since February, budget requests for 2027 have been made. The increase in military spending alone dwarfs the $265 billion cash deficit of Social Security. According to www.whitehouse.gov, the proposed increase in military spending is $445 billion.

Is this a time for lamentations?

I don’t think it’s ever time for lamenting. It’s time to figure out what we can do to protect ourselves.

And realize that our beloved Uncle Sam is a crook.

Related columns:

Scott Burns, “Social Security: The Elephant in the Room,” 12/29/2024: https://scottburns.com/social-security-the-elephant-in-the-room/

Sources and References:

Trustees Report 2025, Table IV.B1 Annual Income Rates, Cost Ratios, and Balances, Calendar Years 1990-2100 (as percent of taxable payroll): https://www.ssa.gov/oact/TR/2025/IV_B_LRest.html#462733

Trustees Report 2025, Table VI.C4.—Operations of the OASI Trust Fund, Fiscal Years 2020-2034 (Dollar amounts in billions): https://www.ssa.gov/oact/TR/2025/VI_C_SRfyproj.html#306103

Trustees Report 2025, Table VI.G9.—OASDI and HI Annual Non-Interest Income, Cost, and Balance in CPI-Indexed 2025 Dollars, Calendar Years 2025-2100 (in billions): https://www.ssa.gov/oact/TR/2025/VI_G3_OASDHI_dollars.html#241156

Trustees Report 2025, Table VI.A1.—Operations of the OASI Trust Fund, Calendar Years 1937-2024: https://www.ssa.gov/oact/TR/2025/VI_A_cyoper_hist.html#282924

Congressional Budget Office, “The Budget and Economic Outlook: 2026 to 2036,” February 2026: https://www.cbo.gov/publication/62105#_idTextAnchor005

This information is distributed for education purposes, and it is not to be construed as an offer, solicitation, recommendation, or endorsement of any particular security, product, or service.

Photo: Scott Burns, 4/24/2026, Sunset in Johnson City, Texas

(c) Scott Burns, 2026

5 thoughts on “How Congress Made Social Security A Small Problem”

Comments are closed.

There is no “Social Security Trust Fund”. It’s a myth, not of pot of money.

See https://www.cato.org/policy-analysis/social-security-trust-fund-myth#:~:text=The%20Social%20Security%20trust%20fund,Security%20Administration%2C%20not%20actual%20money.

Perhaps the most accurate description of the Trust Fund is that it is an accounting artifact, a device to account for excess revenue paid in over expenses and the crediting of that excess with interest. For most of its existence the Trust Fund has held small amounts of credited excess payments, usually measured in a few weeks of payments. The design of the 1984 reforms was to increase the surplus and build a fund that would be available to sustain benefits when the baby boomers retired — now.

If Congress had been able to control other spending rather than increasing spending AND cutting income taxes, the trust fund could have been meaningful. It’s Treasury securities could have been redeemed for cash and that cash could have been borrowed from the public. Instead, federal debt just passed 100 percent of GDP. It’s a long and truly dismal story.

Ronald Reagan and The Great Social Security Heist

The author says that the Social Security amendments passed under Reagan’s presidency laid the foundation for years of embezzlement of the trust funds.

https://www.fedsmith.com/2013/10/11/ronald-reagan-and-the-great-social-security-heist/

The referenced article discusses how and why the Reagan administration implemented an increase in the Social Security tax from a combined 10.8% to 12.4%, with the excess revenue generated going into the Trust Fund (Fund), as a way to “save” Social Security. In reality, the move shifted more of the federal tax burden to lower income and to middle class Americans, while falsely taking credit for “saving” Social Security, as the top income tax rate fell from 70% to 28%, and the excess Social Security tax revenues were used to help reduce the deficit since they counted as income in the unified budget calculations, to offset the cut in top bracket income taxes.

The “Trust Fund” asset that the Social Security Administration (SSA) has is matched dollar for dollar by the liability that the Treasury Department has to made good on the government bonds. Therefore, the net value of the Fund to the federal government has always been zero, and historically, the Fund has been relatively small, just to make sure that that the SSA can make timely payments. A chart in the article showing SSA income, cost, Fund cash flow and Fund total assets illustrates the huge increase in the Fund starting in 1985.

The more honest way to maintain the Pay As You Go system would have been to adjust the Social Security tax to maintain about one year’s worth of benefits in the Fund which was its original purpose, i.e., a cash cushion to make sure that benefits were paid out on a timely basis. Taxpayers could have then invested what they would have paid into the mythical Fund into their own investment accounts. As an example of what we could have done with the excess Social Security taxes is that if one had invested $200 per month (about $7 per day) in the Vanguard S&P 500 Index Fund starting in 1985, one would currently have an investment balance of about $1.4 million. Alternatively, if Social Security had invested the $2.9 Trillion Fund in the Vanguard Index Fund, in equal amounts starting in 1985, the value of the Fund would have been about $40 Trillion, with no effect on benefits paid over the 40 year time frame, since the Fund represents tax revenue, in excess of benefits paid.

Jeffrey,

Thanks for a very succinct summary of what actually happened. There are, alas, lots of ways to do this but most people won’t understand any of them.

I’ve been writing about this for decades both in columns and, more particularly, in two books published by MIT Press. I coauthored “The Coming Generational Storm” with economist Larry Kotlikoff in 2005 and we revisited the topic in 2012 with “The Clash of Generations.”

Kotlikoff, along with economist Alan Auerbach, created generational accounting, a tool for examining how tax payments and benefits are distributed over time. This included a more accurate measurement of the unfunded liabilities of Social Security (not to mention Medicare) than the 75 year balance period that had routinely been used by the Social Security Trustees. Those figures are truly huge!

Some scenarios:

Can taxes alone fix long-term deficits?

Taxes alone would require historically large increases to stabilize long-term federal debt, highlighting the limits of revenue-only solutions

https://www.brookings.edu/articles/can-taxes-alone-fix-long-term-deficits/